7 2: Statement of Cash Flows Business LibreTexts

Category : Bookkeeping

On Propensity’s statement of cash flows, this amount is shown in the Cash Flows from Operating Activities section as Gain on Sale of Plant Assets. Investing and financing transactions are critical activities of business, and they often represent significant amounts of company equity, either as sources or uses of cash. Common activities that must be reported as investing activities are purchases of land, equipment, stocks, and bonds, while financing activities normally relate to the company’s funding sources, namely, creditors and investors. These financing activities could include transactions such as borrowing or repaying notes payable, issuing or retiring bonds payable, or issuing stock or reacquiring treasury stock, to name a few instances.

How confident are you in your long term financial plan?

In other words, changes in asset and liability accounts that affect cash balances throughout the year are added to or subtracted from net income at the end of the period to arrive at the operating cash flow. Cash flows from financing activities always relate to either long-term debt or equity transactions and may involve increases or decreases in cash relating to these transactions. Stockholders’ equity transactions, like stock issuance, dividend payments, and treasury stock buybacks are very common financing activities. Debt transactions, such as issuance of bonds payable or notes payable, and the related principal payback of them, are also frequent financing events. Changes in long-term liabilities and equity for the period can be identified in the Noncurrent Liabilities section and the Stockholders’ Equity section of the company’s Comparative Balance Sheet, and in the retained earnings statement.

Cash Flow from Investing Activities

Thus, the decrease in receivable identifies that more cash was collected than was reported as revenue on the income statement. Thus, an addback is necessary to calculate the cash flow from operating activities. Companies tend to prefer the indirect presentation to the direct method because the information needed to create this report is readily available in any accounting system. In fact, you don’t even need to go into the bookkeeping software to create this report. Let’s take a look at the format and how to prepare an indirect method cash flow statement. Net cash flow from operating activities is the net income of the company, adjusted to reflect the cash impact of operating activities.

Accounting Research Online

Decreases in current liabilities indicate a decrease in cash relating to (1) accrued expenses, or (2) deferred revenues. In the first instance, cash would have been expended to accomplish a decrease in liabilities arising from accrued expenses, yet these cash payments would not be reflected in the net income on the income statement. In the second instance, a decrease in deferred revenue means that some revenue would have been reported on the income statement that was collected in a previous period. To reconcile net income to cash flow from operating activities, subtract decreases in current liabilities.

Financing activities pertain to sources of funding, and includes the receipt of the funds and the repayment thereof. A financial professional will offer guidance based on the information provided and offer a no-obligation the difference between fixed and variable costs call to better understand your situation. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

Part 2: Your Current Nest Egg

On the same day you pay your cell phone bill and car insurance payment for a total of $210. The net cash inflow on that day is $160; that is, $160 more came in than went out. Also, in 2023, the FASB kicked off a project to make targeted improvements to the statement. The cash flow statement does not replace the income statement as it only focuses on changes in cash. In contrast, the income statement is important as it provides information about the profitability of a company.

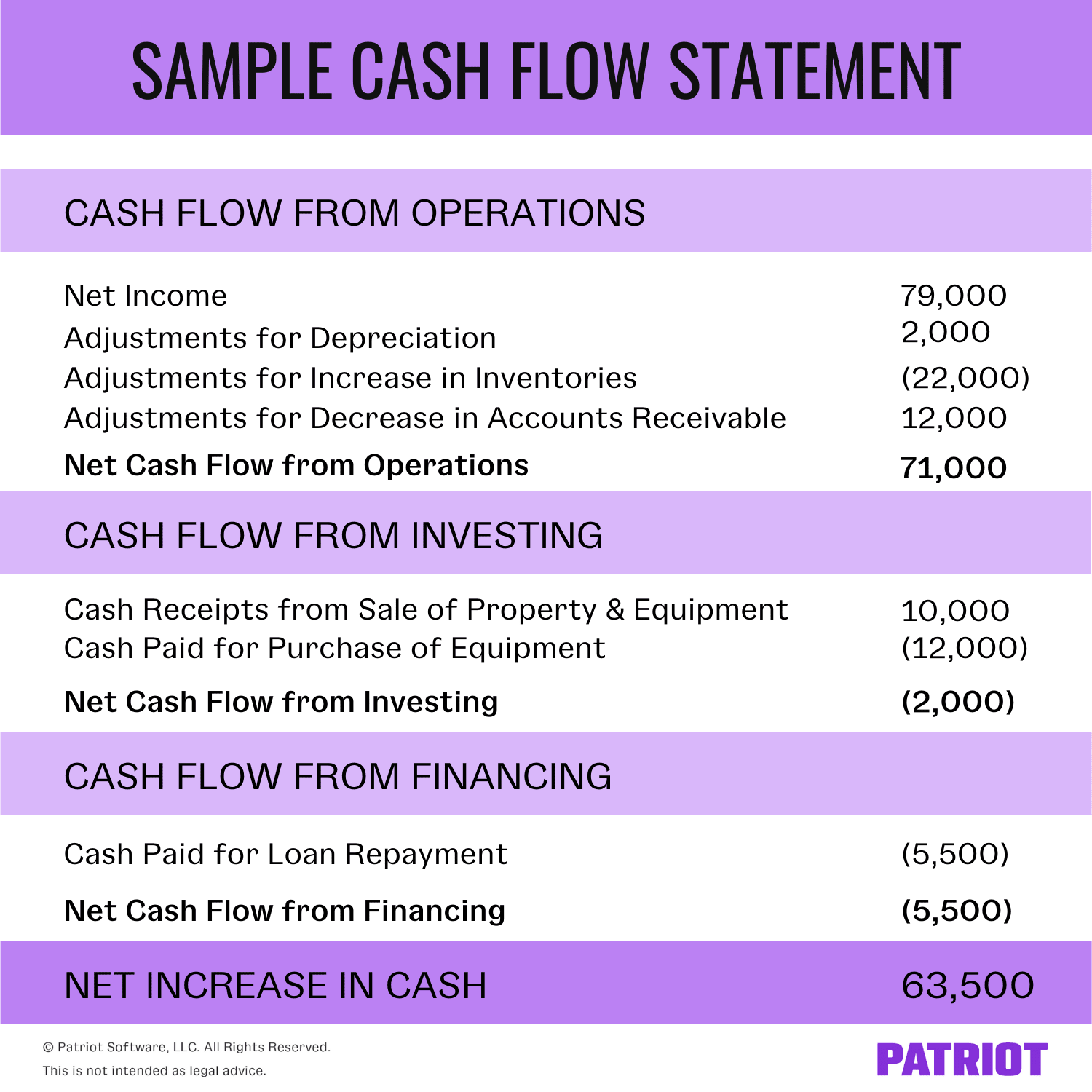

The operating activities cash flow is based on the company’s net income, with adjustments for items that affect cash differently than they affect net income. The net income on the Propensity Company income statement for December 31, 2018, is $4,340. On Propensity’s statement of cash flows, this amount is shown in the Cash Flows from Operating Activities section as Net Income. The cash flow statement is an essential financial statement for any business as it provides critical information regarding cash inflows and outflows of the company.

- Changes in long-term assets for the period can be identified in the Noncurrent Assets section of the company’s comparative balance sheet, combined with any related gain or loss that is included on the income statement.

- As a result, the business has a total of $126,475 in net cash flow at the end of the year.

- Therefore, it does not evaluate the profitability of a company as it does not consider all costs or revenues.

- The magnitude of the net cash flow, if large, suggests a comfortable cash flow cushion, while a smaller net cash flow would signify an uneasy comfort cash flow zone.

- For example, in the Propensity Company example, there was a decrease in cash for the period relating to a simple purchase of new plant assets, in the amount of $60,000.

Calculate net cash flows from investing activities amount by deducting cash outflows from cash inflows. This final summary amount indicates that $28,000 more “came in” than was paid out during this year for investing activities. (If it were a net cash outflow, use parenthesis to indicate this.) This is the second of six numbers in the right-hand column.

All of these adjustments are totaled to adjust the net income for the period to match the cash provided by operating activities. Using the basic shell that includes the heading and formatting captions, complete the statement of cash flows. Therefore, it should always be used in unison with the income statement and balance sheet to get a complete financial overview of the company. The cash flow statement is useful when analyzing changes in cash flow from one period to the next as it gives investors an idea of how the company is performing.

They can be calculated using the beginning and ending balances of various asset and liability accounts and assessing their net decrease or increase. This section records the cash flow between the company, its shareholders, investors, and creditors. It might be helpful to look at an example of what the indirect method actually looks like. A Statement of Cash Flows (or Cash Flow Statement) shows the movement in the Cash account of a company.